Depreciation

is a part of the cost calculation with the engineering formula.

It considers the loss of value of a working system during its life span.

Imagine you plan

to buy a machine. It is very expensive, so the decision should be made

carefully. If you intend to get a loan from the

bank, you need a plan to pay the money back within a certain time. That means:

Hour by hour you must put aside a certain sum, which you will transfer to your

bank at the end of the month.We call this depreciation.

The lifetime of a

tool or machine is limited. There are several reasons for decay:

• Technical decay (obsolescence) depends

on technical progress: when new and better machines appear, your old machine

may be no longer competitive.

• Technical aging (wear) happens when

parts of the machine become thin, stiff, inflexible, and break, i.e.

• In some situations, we have only limited

use of a machine, afterwards we will not need it

any longer.

• Or the machine suffers from a “fashion

change”, when your technology will become unfashionable, and nobody will be

interested in this technology any longer.

Depreciation is

the response to the progressive loss of value of your machine. During this

time, we must pay back the initial investment.

If we did not

borrow the money from the bank, we have taken it from the “investment pool” of

our company. We have only changed money into a machine with the same value.

When the value of the machine decreases, we must pay back into this pool in

order to stay as “rich” as before.

A third argument

for depreciation deals with taxes:

Since the taxes

are based on the win, we should not forget the hidden costs by the daily

devaluation of our equipment.

How do we

calculate depreciation?

• First, we decide how many years the

machine will be used.

• Then we ask, whether it will be possible

to sell the old machine at the end of the utilization time. But be careful

there! Normally there is some residual value, but we may want to assume that it

is 0 and use it as a silent reserve to compensate the higher price for a new

machine – due to inflation and technical development.

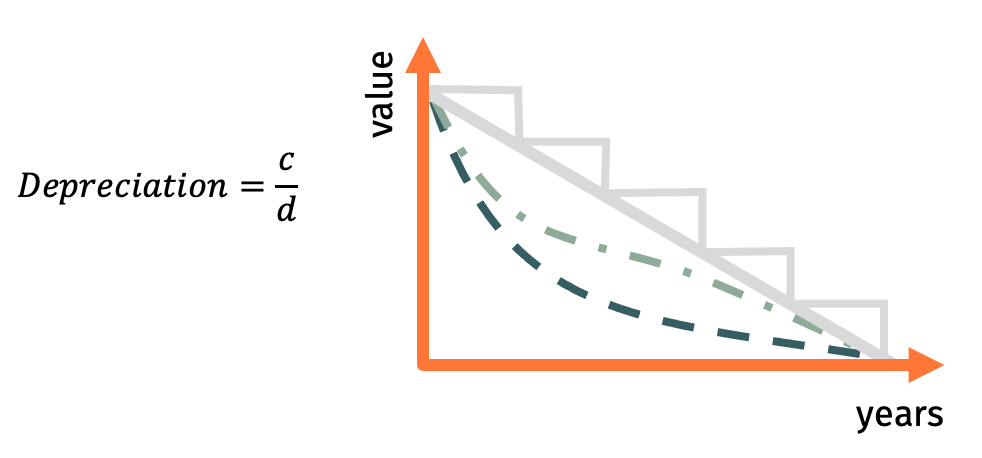

• The annual depreciation now is

calculated as the initial investment minus the assumed residual value divided

by the number of years.

This is called

linear depreciation. In fact, real devaluation is not linear (here implied with

red or green) but in practical term a linear solution is good enough and it is

easier to calculate.